When Is My Property Tax Assessed?

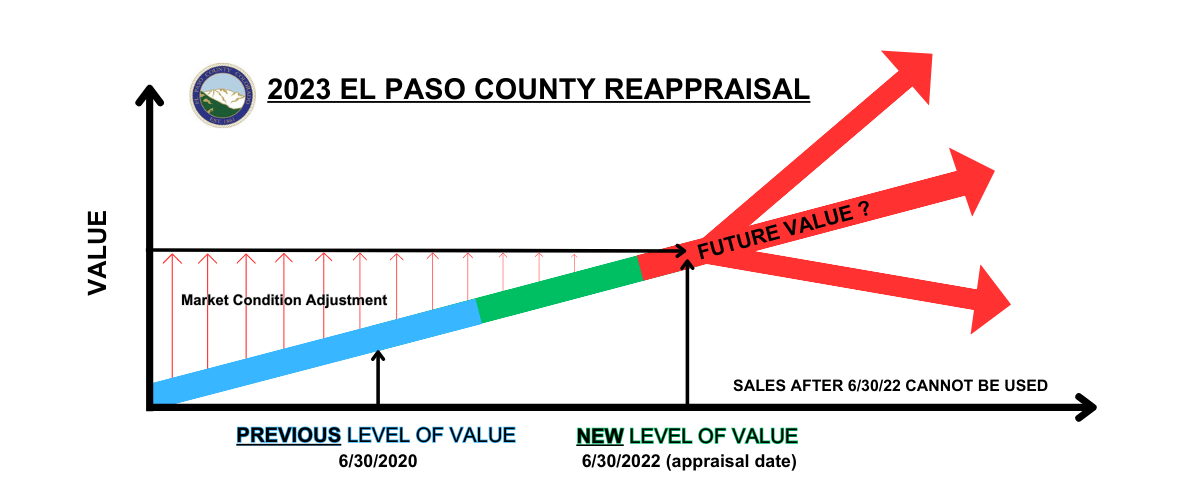

Under Colorado Law, real property must be re-appraised every 2 years, which occurs each odd-numbered year (2021, 2023, 2025, etc.). The Assessor's Office studies the sales of properties sold during the statutory 18-month study period ending June 30th of the year prior to the reappraisal. The new 2023 values will be based on properties sold between Jan 1, 2023, and June 30, 2024. Properties are valued based on their existing characteristics or state of completion as of each January 1st. Thus, the Appraisal Date (June 30, 2024) is based on sales during the study period and the effective date used to determine value. The Assessment Date is based on the property's condition as of January 1st. New construction, for example, may be 50% complete on January 1st, and will be valued accordingly.

Many homeowners were shocked to open their assessment to find that their taxes had increased (on average) about 44%. Homeowners are confused by the valuation the Assessor placed on their home; they feel like that price is not what they could sell their home for today. And they’re not wrong, as values have softened to the tune of 5-10% since that date. However, the assessment period of Jan 1, 2023 – June 30, 2024 catches home values at the height of our market. Essentially, the question homeowners should ask themselves is “What could you have sold your home for at that point in time” to better understand the high valuation provided.

How Are My Property Taxes Calculated?

The Assessor's Office is tasked with establishing fair and equitable valuations and DOES NOT set property taxes or collect payments. The following formula is used to determine property taxes:

- The Assessor 'Actual Value' is adjusted by the appropriate Assessment Rate, which varies depending on the property type.

-

- multi-family housing and all other residential property (single-family) are multiplied by 6.765% (0.06765)

- hotels, motels, and B&Bs are multiplied by 27.9% (0.279),

- renewable energy production and agricultural property are multiplied by 26.4% (0.264),

- commercial, vacant land, and industry are multiplied by 27.9% (0.279),

For example, (using a home valued at median average):

- Next, the Assessed Value, less any exempted amount, is multiplied by the applicable Tax Rate, which is expressed as a decimal fraction of a dollar for every one dollar of Assessed Value in Colorado. This is known as millage or mills, with one mill being 1/1,000th of a dollar or 0.001 (1/10th of a penny).

For our example, using an average 80 mills:

Calculation Example:

|

Actual Value |

Assessment Rate | Assessed Value | Mill Levy | Est. Taxes |

|

$500,000 (Residential) |

6.765% | $33,825 | 80 Mills | $2,706 |

|

$500,000 (Commerical/Vacant Land) |

27.9% | $139,500 | 80 Mills | $11,160 |

How Is My Property Asssessed?

Residential

The Assessor appraisers use the Sales Comparison (Market) Approach to study the sales of homes similar to yours, which were sold within a specific 18-month time frame, from Jan 1, 2023, to June 30, 2024. This approach involves comparing your property to recently sold properties in the same or similar neighborhoods, with similar characteristics, such as size, age, condition, and features. Based on this analysis, the appraisers determine the fair market value of your property, which is used to establish the assessed value for tax purposes through a Mass Appraisal Process.

Will My Property Taxes Go Up?

Not necessarily. In Colorado, the Taxpayer's Bill of Rights (TABOR) Amendment limits the amount of revenue that the state government can collect and spend each year, based on the rate of inflation and population growth. This amendment requires that all tax increases, including property tax mill levy increases, must be approved by the voters. It also mandates that all tax revenue above the state's TABOR limit must be refunded to taxpayers, unless voters approve an exemption to keep the revenue for specific purposes.

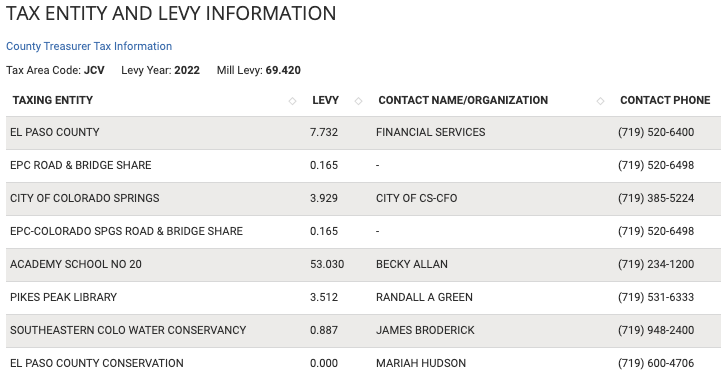

The Assessor does not set property taxes or mill rates, and in Colorado, residential and non-residential assessment rates are set by the State Legislature. The mill rates for local taxing entities, such as the city, county, school districts, fire districts, library, and others, are provided in mid-December, and it is the elected members of these taxing authority boards who determine their yearly mill levy for their following year budgets.

You can find information regarding Mill Levy’s at the El Paso Treasurer’s website. You can also see specific Tax Entity and Levy Information on a specific property by entering a property address into the parcel search tool on the Assessors website.

Appealing Your Property Value

As a property owner, you have the right to appeal the assessed value of your property if you believe it is incorrect. When you receive your Notice of Valuation (NOV) from the county Assessor's Office, there will be instructions explaining how to submit an appeal, which can be done in writing, in person, or online.

When submitting an appeal, it is important to explain why you believe your property value is incorrect and provide supporting documentation to assist the appraiser in making a review of your value. This could include sales of similar properties, information about condition problems with your property, or any other relevant information that supports your appeal.

After receiving your appeal, the county assessor's office will review your documentation and make a determination regarding your property value. If your appeal is approved, the assessed value of your property will be adjusted accordingly, which may result in a lower property tax bill.

Appealing Your Property Value

As a property owner, you have the right to appeal the assessed value of your property if you believe it is incorrect. When you receive your Notice of Valuation (NOV) from the county Assessor's Office, there will be instructions explaining how to submit an appeal, which can be done in writing, in person, or online.

- Fill out the form sent and mail back

- Deliver to the office in person

1675 W. Garden of the Gods, Ste #2300, Colorado Springs, CO 80907 - Call 719-520-6600

- Visit the website and file online

It is the responsibility of the property owner to furnish good information about your property to the Assessor. If you plan to file an appeal, it is important that you understand

- How the Assessor values property

- How to gather information about your property and similar properties (comparables)

- How the appeals process works and what the deadlines are

If you would like a licensed REALTOR® to assist you with the process or supplying comparable data, please contact us!

Appealings Process and Tips

When submitting an appeal, it is important to explain why you believe your property value is incorrect and provide supporting documentation to assist the appraiser in making a review of your value. This could include sales of similar properties, information about condition problems with your property, or any other relevant information that supports your appeal.

After receiving your appeal, the county assessor's office will review your documentation and make a determination regarding your property value. If your appeal is rejected, you have the opportunity to file with Clerk of County Board of Equalization. If your appeal is approved, the assessed value of your property will be adjusted accordingly, which may result in a lower property tax bill.

Who makes a good candidate for appeal? Note that many homes in a developed homogeneous track neighborhood may be close to properly valued. Consider a bell curve; those homes are going to fall into the greatest 2/3rds of the bell. But some outliers that may be ripe for revaluation include unique/custom properties (Old North End), properties on land (Black Forest) or with unique buildings/pools/etc, or of poorer condition than the majority of homes surrounding (ie 1960 home with original finishes near or adjacent to new community or construction). They will consider Cost to Cure for those properties that require a large sum of money to bring it up to condition to meet the proposed value. New builds are not treated the same as resale, and may be a good candidate for reevaluation.

Here is a sample of potential tax savings evaluations:

|

Reduction Value |

Assessment Rate | Mill Levy | Tax Savings |

|

10,000 |

6.765% | 80 Mills | $54.12 |

|

10,000 |

6.765% | 100 Mills | $67.65 |

|

10,000 |

6.765% | 120 Mills | $81.18 |

|

50,000 |

6.765% | 80 Mills | $270.60 |

|

50,000 |

6.765% | 100 Mills | $338.25 |

|

50,000 |

6.765% | 120 Mills | $405.90 |

Our REALTORS® Would Love to Assist You!

But if you prefer to proceed independently, here are some steps below to help you.

Steps To Appeal Your Property Tax Assessment

- Visit the Parcel Search page: https://property.spatialest.com/co/elpaso/#/

- Enter the property address

- Use the ‘COMPER’ tool

- The tool will default to certain filters. You will want to find properties of like size, year build, home type, condition, and proximity/neighborhood. You can click the ‘Add Comp’ button if you would like it to be included.

- They are looking for 3-6 comparable properties to evaluate.

- Note that you must consider the ‘Time Adj. Sale Price’ in your valuation, NOT the value as highlighted in green.

- The date of valuation is June 30, 2024. Therefore, if a home sold in the prior months, the Time Adjustment as noted on the Time Trends document is applied to that sale price month over month up to valuation date. That ranged from 1-1.7% across the 20 economic areas in the county. This number is an appreciation per month used to adjust value.

- The tool will default to certain filters. You will want to find properties of like size, year build, home type, condition, and proximity/neighborhood. You can click the ‘Add Comp’ button if you would like it to be included.

- Use the 'APPEAL' tab to begin the online process.

- You will fill out contact information, include comps (saved through tool or provided from another source, upload any supporting documents, explain why you feel the value is too high, and submit.

- Be sure you are clear in your documentation, with little opinion and supported facts.

|

|